By Pablo Tascon

Permanent establishment risk is the chance that your company’s activities in another country could accidentally create a taxable presence there, forcing you to pay local corporate taxes. It’s an invisible tripwire for any business hiring internationally or growing its global footprint. The risk isn't about having a physical office—it's determined by the substance of your operations.

Your Company's Unseen Tax Footprint

Think of your business as leaving a footprint wherever it operates. Some footprints are obvious, like a registered branch or a factory. But others are much harder to see, even though they're just as significant to tax authorities. This "tax footprint" is the core idea behind permanent establishment (PE).

Once your activities in another country become substantial enough, you create a PE. This acts as a trigger, switching on local corporate tax obligations you might not have known you had.

This concept is no longer a niche concern—it’s critical for any business with cross-border operations. Whether you have a single employee working remotely from another country or a sales agent closing deals abroad, you could be creating permanent establishment risk without realizing it. The rules aren't based on your intentions; they're based on the nature and continuity of your business activities.

Why This Matters More Than Ever

In today's borderless economy, understanding permanent establishment is non-negotiable. The explosion of remote work and global teams has blurred the old lines, making it easier than ever to stumble into a taxable presence. A single key employee working from their home office in another country could be all it takes to trigger PE.

Ignoring this risk can backfire badly. The consequences often include:

- Surprise Tax Bills: You could be on the hook for back taxes in a foreign country, often stretching back several years.

- Heavy Penalties: Tax authorities don't take kindly to unpaid corporate taxes. They often impose steep fines and high interest charges on top of what you owe.

- Operational Headaches: A foreign tax dispute is a massive drain on your time, money, and focus, pulling you away from running your business.

- Reputational Damage: Non-compliance can tarnish your company's reputation and put up roadblocks to future global expansion.

The key takeaway here is that PE is about economic substance over legal form. Tax authorities are trained to look past your contracts and formal structures to see what your business is actually doing in their country.

From Bricks to Clicks

It used to be that a "fixed place of business," like a branch or a workshop, was the main trigger for permanent establishment. Not anymore. The definition has expanded to keep up with how we work today.

A consistent workspace in a co-working facility, a long-term construction project, or even an agent with the authority to sign contracts on your behalf can now create a PE.

This guide will break down the specific triggers, explain the key exemptions, and give you practical strategies to manage your permanent establishment risk. Understanding your company’s global tax footprint is the first step toward confident, compliant international growth.

The Core Triggers of Permanent Establishment

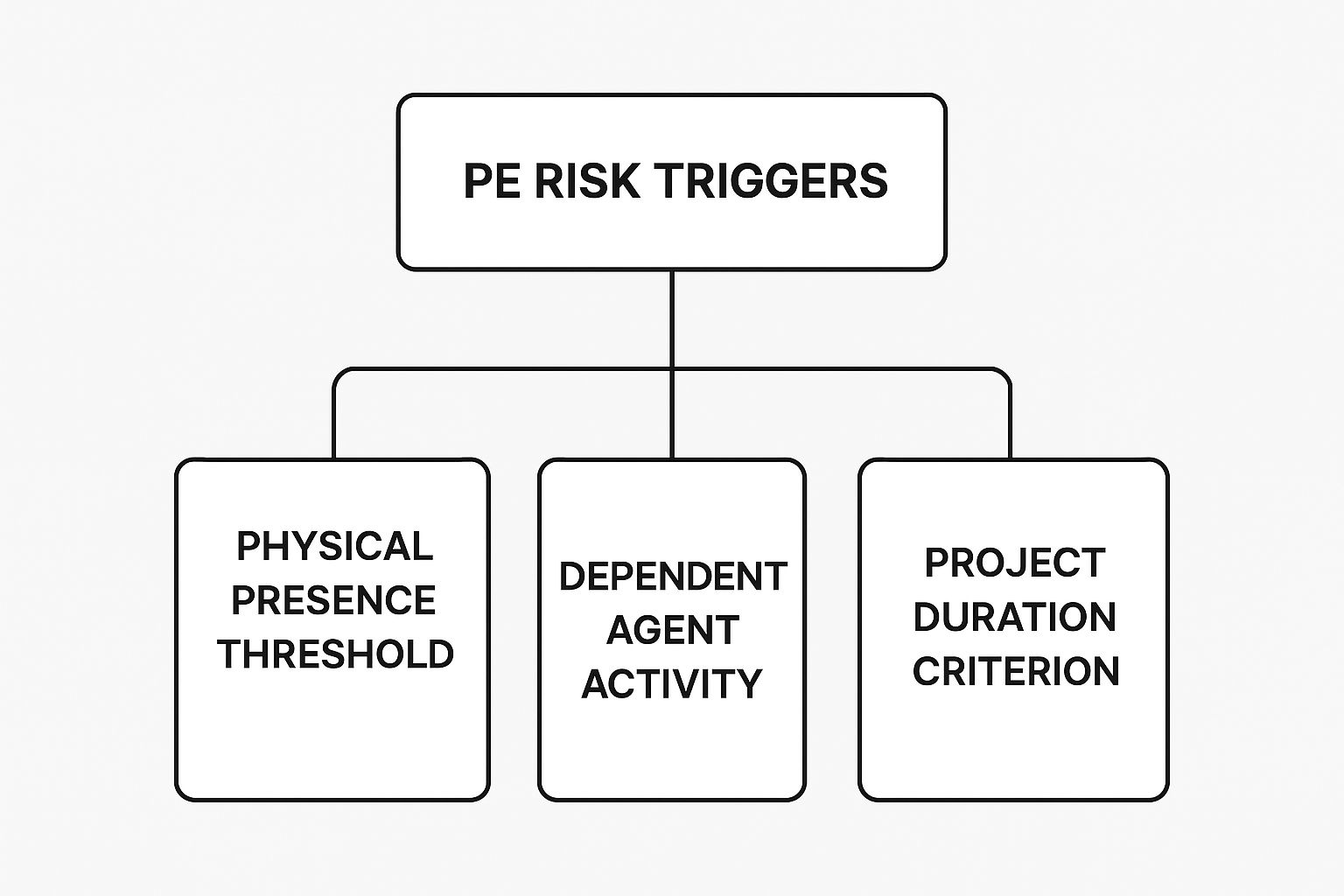

To get a handle on permanent establishment risk, you first need to know what puts it in motion. Tax authorities are always on the lookout for specific patterns that signal a company has a stable and significant business presence in their country. While the rulebook changes from one jurisdiction to the next, the game generally revolves around two core ideas: having a fixed place of business and the actions of your agents on the ground.

Don't think of these as single tripwires. Instead, picture them as a collection of signals that, when viewed together, paint a clear picture of your company's economic footprint abroad. Spotting these signals in your own operations is the first—and most critical—step toward smart, proactive compliance.

This visual breaks down the main categories of activity that tax authorities zoom in on when they're sniffing out permanent establishment risk.

As you can see, the risk isn't about just one thing. It's a mix of your physical presence, the authority your people have, and how long your projects last. These are all key factors in the eyes of international tax law.

Fixed Place of Business PE

The most classic trigger is the fixed place of business. This is any physical spot where your company's business is regularly carried on, whether in whole or in part. An office, factory, or shop are the obvious ones, but the definition has stretched a lot in our modern, flexible working world.

Today, a fixed place of business can also mean:

- A dedicated desk in a co-working space: If your employee consistently uses the same desk, tax authorities could argue that spot is at your company's disposal.

- An employee's home office: This is a huge area of growing scrutiny. If an employee's home is central to your revenue-generating work, or if you chip in for their office expenses, it could be flagged as a PE.

- Project sites: A construction or installation site that runs beyond a certain timeframe (often six or twelve months, depending on the local tax treaty) will almost always create a PE.

The real test is whether the location has a degree of permanence and is effectively at your company's disposal. It doesn’t matter if you legally own or rent the space. What matters is your control over it for business purposes.

Agency PE: The Human Element

Even without a physical office, your company can still create a permanent establishment risk through the actions of your people. This is called Agency PE, and it happens when someone acting on your behalf in another country creates a taxable presence for you just by doing their job.

This trigger usually involves what’s known as a dependent agent. This is just a person or company that works for you with a high degree of reliance—think an employee or a contractor who only works for you. If this agent has the authority to close deals in your company’s name and does so regularly, they can trigger a PE all on their own. The substance of their role is what counts. To get deeper into the legal side of this, take a look at our guide on understanding the definition of contracted services.

Imagine a software company with a sales director based in Germany. If she routinely negotiates and signs contracts with German customers on the company's behalf, her actions alone could create a taxable presence there—even if the company has zero office space in the country.

The critical line is drawn between a dependent agent and an independent one. An independent agent, like a broker who represents lots of different companies, usually won't create a PE for their clients because they are acting in the ordinary course of their own business. But an agent who works almost exclusively for you and is economically dependent on your company? That’s a whole different story.

To help clarify which activities are more likely to catch a tax authority's eye, it’s useful to see them laid out by risk level.

Common PE Triggers and Their Risk Levels

The table below breaks down common business activities and assigns a typical risk level to each. This should give you a quick way to gauge where your operations might be creating exposure.

| Business Activity | Description | Typical PE Risk Level |

|---|---|---|

| Warehousing for Storage | Maintaining a warehouse solely for storing, displaying, or delivering your own goods. | Low |

| Purchasing Office | An office dedicated exclusively to buying goods or merchandise for the company. | Low |

| Data Collection | A location used only for collecting information (e.g., market research). | Low |

| Employee Home Office | An employee working from home, especially if the role is core to the business. | Medium to High |

| Long-Term Project Site | A construction or installation project lasting more than 6-12 months. | High |

| Sales Agent Closing Deals | A dependent agent who regularly negotiates and finalizes contracts. | High |

| Local Management Office | A branch or office where key management decisions are made. | High |

As you can see, the risk really climbs when the activities move from being preparatory or auxiliary to being part of the core, revenue-generating engine of your business. That’s the line tax authorities care about most.

Understanding Key Exemptions and Safe Harbors

While the triggers for permanent establishment risk seem broad, international tax treaties thankfully offer some specific exemptions. These are often called "safe harbors"—activities you can carry out in a foreign country without accidentally creating a taxable presence.

Getting a handle on these rules is absolutely crucial for structuring your global operations. Think of it this way: not every footprint you leave in another country is deep enough to get the tax authorities interested. The whole point of these exemptions is to let businesses explore new markets and handle logistics without getting hit with an immediate tax bill.

The Preparatory or Auxiliary Activities Exemption

The biggest and most important safe harbor is for activities that are preparatory or auxiliary in nature. In simple terms, this means the work being done in the foreign country isn't your core, money-making business. It's just supporting the main show happening somewhere else.

This distinction is the bedrock of most PE risk mitigation strategies. A company scouting a new market is doing something very different from one that's actively closing deals there. One is preparation; the other is the core business. Tax authorities always look at the substance of what you’re doing, not just the label you put on it.

So, what counts as preparatory or auxiliary? The guidelines are a bit flexible, but they generally cover anything that’s a step removed from the actual sales process.

These safe harbor activities are designed to allow businesses to dip their toes in a new market without being pulled into the local tax system. The moment these activities cross the line and start directly contributing to profits, the exemption disappears.

Common Safe Harbor Examples

To make this more concrete, here are a few classic examples of activities that usually fall under the preparatory or auxiliary exemption. On their own, these won't create a permanent establishment.

- Storing and Delivering Goods: Using a warehouse in another country just to store, display, or deliver your own products is a classic safe harbor. The crucial detail is that no sales are actually happening at that location.

- Purchasing Goods or Information: Setting up an office that does nothing but buy goods or gather market research for your company is also typically exempt. It supports the main business but doesn't generate income on its own.

- Advertising and Promotion: You can run general advertising campaigns or promotional activities to build brand awareness without triggering a PE, as long as you aren’t concluding contracts there.

- Purely Administrative Tasks: A small office that only handles internal admin—like payroll for your expatriate staff or internal communications—will almost always qualify for the exemption.

This isn't an exhaustive list, and it's worth noting that combining several "safe" activities can sometimes be viewed differently by tax authorities. Still, it gives you a solid framework for what's considered low-risk.

Time-Based Exemptions for Specific Projects

There's another important safe harbor that's all about the clock, especially for construction and installation projects. Many tax treaties offer a specific time-based exemption, creating a clear deadline for when a project site officially becomes a PE.

This grace period is often six months, though some treaties are more generous and extend it to 12 months or even longer. If your construction site, assembly project, or a similar job is wrapped up within that timeframe, you won't trigger a PE.

But you have to be careful here. This is a hard deadline. If the project runs even one day over the period specified in the treaty, the PE is usually considered to have existed from day one. That can expose your company to a world of pain in the form of back taxes and penalties. Tight project management isn't just good business—it's essential for staying in the clear.

The Consequences of Ignoring PE Risk

So, we've talked about the theory. Now let’s get real about what happens when a company gets this wrong. Overlooking permanent establishment risk isn't about minor paperwork headaches; it's about facing serious financial and operational blows that can completely derail a growing business.

When tax authorities decide your business has an undeclared PE, the first thing they do is demand back taxes. And they don't just look at the current year. They can—and often do—go back several years, calculating all the corporate income tax you should have paid on profits from your in-country activities.

On top of that, they'll tack on interest charges for every day the payment was late, which adds up fast. But the financial pain doesn’t stop there. The penalties for non-compliance can be punishingly high.

Financial Penalties and Reputational Damage

Penalties for an undeclared PE can run anywhere from 5% to 20% of the owed tax liability, turning a bad situation into a catastrophic one. These numbers alone should make it clear why proactive PE risk assessments are so important. It's why many companies turn to solutions like an Employer of Record (EOR) or meticulously structure their operations to avoid tripping these wires. You can dig deeper into how businesses are handling these challenges by reading these insights on PE risk management.

Beyond the money, an investigation can freeze your operations, poison key business relationships, and ignite a public relations firestorm. A surprise seven-figure tax bill is exactly the kind of thing that spooks investors and tarnishes your reputation, making every future expansion effort that much harder.

Proactive compliance isn't just a legal formality; it's a strategic necessity for sustainable global growth. Ignoring permanent establishment risk is like building a global enterprise on a shaky foundation—it’s only a matter of time before cracks appear.

Case Study: A Software Company's Costly Oversight

To see just how quickly this can all go sideways, let’s look at the story of "Innovatech," a fast-growing software company from the U.S. Eager to break into the European market, Innovatech hired three senior sales executives in Germany, Spain, and France.

The execs all worked from their home offices, and Innovatech didn't have a legal entity anywhere in Europe. Crucially, they were authorized to negotiate pricing, terms, and finalize contracts with major European clients directly on Innovatech’s behalf. For two years, the strategy was a home run, bringing in millions in new revenue.

The trouble started when a German tax authority did a routine audit on a local partner and noticed large, regular payments going to a U.S. company. That single thread was enough to trigger a full-blown investigation into Innovatech's European operations.

The Unraveling

German tax authorities concluded that the sales executive—who routinely closed deals from his home office—was a dependent agent. His actions single-handedly created an Agency PE. This ruling set off a domino effect, sparking similar investigations in Spain and France, both of which came to the same conclusion.

The consequences for Innovatech were catastrophic:

- Massive Tax Bill: The company was hit with a bill for three years of back taxes on all profits from its German sales. Once interest and penalties were added, the final amount owed was over $1.2 million in Germany alone.

- Operational Chaos: Authorities in Spain and France quickly followed suit. Innovatech found itself fighting a multi-front legal battle that drained its resources and distracted management for months. They had to hire expensive local tax advisors in three different countries.

- Reputational Fallout: News of the tax dispute went public, spooking investors and alarming key European clients. The ordeal painted Innovatech as either careless or deliberately evasive, shredding its credibility in a market it desperately needed to win.

Innovatech’s story is a stark reminder of how easily permanent establishment risk can be triggered. The company’s mistake wasn't malicious; it was a simple failure to align its aggressive growth strategy with international tax law. What began as an agile, low-cost way to enter a market ended in a seven-figure liability and a major setback to its global ambitions.

How to Mitigate Permanent Establishment Risk

Knowing what permanent establishment risk is and what triggers it is one thing. Actually stopping it from happening is a whole different ball game. If you want to expand globally without a surprise tax bill showing up, you have to be proactive. Luckily, there are a handful of smart, actionable strategies that can build a strong defense so you can operate with confidence.

Think of these strategies less as restrictions and more as a playbook for intelligent global growth. The goal isn't to avoid expansion; it's to expand in a way that’s smart, deliberate, and fully aware of the international tax lines you can't cross.

This all comes down to a mix of careful assessments, the right legal structures, and crystal-clear internal policies. Nail these, and you'll dramatically lower your company's exposure and build an international footprint that’s built to last.

Conduct a PE Risk Assessment

Before you even think about making a major move into a new country, your very first step must be a thorough permanent establishment risk assessment. This isn’t just a formality or a box-ticking exercise. It's a deep dive into how local tax authorities are going to view your planned activities on the ground.

This assessment needs to pull apart every single aspect of your proposed operations. Are you getting a physical office? What are your employees or contractors actually going to be doing there? How long will your projects run? Answering these questions with total honesty is what gives you the clarity to spot red flags before they turn into serious problems.

A proper PE risk assessment is your strategic map. It shows you where the safe terrain is and flags the danger zones where you need to tread very carefully—or find another route entirely.

This initial review is the absolute foundation of your entire mitigation strategy. It helps you customize your approach for each country, because what's considered low-risk in one place could be a massive PE trigger somewhere else.

Structure Employment Contracts to Limit Authority

One of the fastest ways to accidentally create an Agency PE is to give an employee or agent abroad the power to sign deals on your behalf. To head this off, you have to meticulously structure employment and contractor agreements to clearly define—and limit—their authority.

The exact wording in these contracts is everything. They should state, in no uncertain terms, that the individual does not have the authority to negotiate core terms or finalize contracts in the name of your parent company. Their role should be framed around things like promotion, generating leads, or managing client relationships, with the final contract approval always happening back in your home country. For more on creating solid agreements, our insights on managing contract risk are a great place to start.

But this isn't just about what’s written down. Tax authorities look at substance over form, so your day-to-day operations have to actually reflect these contractual limits.

Differentiate Between Agents

Drawing a bright line between dependent and independent agents is another cornerstone of managing permanent establishment risk. An independent agent—like a broker who represents several different companies—is just acting in the ordinary course of their own business. They're far less likely to create a PE for you.

A dependent agent, on the other hand, works almost exclusively for you and is economically tethered to your company. Their actions are seen as a direct extension of your business.

To keep that separation clear, make sure any agents you work with:

- Represent multiple clients and aren't getting all their income from your business.

- Operate under their own name and carry their own business risks.

- Have the freedom to run their business as they see fit, without you micromanaging them.

Use Smart Legal Structures

Maybe the most powerful way to build a protective wall is to use the right legal structure in the foreign country. Just hiring remote employees or contractors directly from your parent company offers zero insulation. Two much better alternatives can give you the separation you need.

-

Establish a Subsidiary: This is a robust, long-term solution. You create a legally distinct subsidiary in the new country, which becomes its own taxable entity. As long as it operates with genuine independence and any transactions with the parent company are done at "arm's length," it effectively shields the parent from creating a PE.

-

Use an Employer of Record (EOR): If you want to hire abroad without the headache of setting up a whole new legal entity, an Employer of Record is a fantastic option. An EOR legally employs the person for you, taking care of local payroll, taxes, and compliance. Since the worker is officially employed by the EOR—not your parent company—it cuts the direct link that could trigger a PE.

Both of these options create a critical buffer between your core business and the foreign tax authorities, letting you grow your team around the world while keeping your tax footprint exactly where you want it.

How Remote Work Is Reshaping PE Risk

The global shift to remote work has completely upended the traditional rules of permanent establishment risk. What started as a temporary fix is now a core part of the modern economy, forcing tax authorities everywhere to ask a tough question: what does a "fixed place of business" really mean anymore? This new reality is creating complex, unfamiliar challenges for businesses with distributed teams.

A company's PE risk no longer comes down to just having a physical office or branch. Today, the home office of a single, high-value employee in another country can be enough to trigger a full-blown tax investigation. This is a fundamental change in how international tax law is being interpreted and enforced.

The Home Office as a Corporate Outpost

So, when does a simple home office cross the line and become a corporate PE? Tax authorities don't have a single checklist, but they look closely at several factors, zeroing in on the employee's role and the company's influence over the space.

It often boils down to a few key questions:

- Employee Seniority: A senior executive making strategic decisions from their home office is viewed very differently than a junior employee handling administrative tasks.

- Business Criticality: If the work being done from that home office is essential to the company's main revenue streams, the risk of it being classified as a PE skyrockets.

- Company Control: Does the company pay for the home office setup? Is the address listed on business cards or the company website? Does the company require the employee to work from that specific location? Any of these can suggest the space is effectively at the company’s disposal.

With work patterns changing so fast, even home offices used regularly by foreign employees or contractors are drawing more and more scrutiny from tax authorities as potential PEs. It’s a clear signal that risk isn't just about physical assets anymore—it's about the authority and value being generated remotely.

The Emerging Threat of Digital PE

Beyond the home office, an even more abstract concept is taking hold: Digital Permanent Establishment. This idea throws out the traditional need for any physical presence at all. A growing number of countries are now arguing that a significant and sustained digital footprint inside their borders is enough to create a taxable entity.

A Digital PE could be triggered by significant revenue from digital sales to customers in a specific country, extensive user data collection, or targeted online advertising, even without a single employee or office on the ground.

This isn't just a futuristic concept; it's a direct response to the business models of Big Tech, but the ripple effects will eventually hit any modern, tech-driven business. It shows that tax authorities are determined to capture revenue from economic activity happening within their borders, no matter how it’s conducted. This makes a robust risk assessment essential. For complex cross-border situations, performing the right kind of due diligence service is critical.

This shift means companies can no longer hide behind a lack of a physical footprint to avoid permanent establishment risk. The very definition of "presence" is expanding, making proactive planning more critical than ever for any business navigating the future of work.

At Tascon Legal & Ediscovery, we specialize in helping businesses navigate the complexities of cross-border compliance and risk management. We provide expert guidance on international legal frameworks to ensure your global expansion is built on a solid, compliant foundation. Learn how we can protect your business by visiting us at https://tasconlegal.com.