by Pablo Tascon

The audit committee's fundamental role is to provide independent oversight of a company's financial reporting processes, internal controls, and external auditors.

At its core, the committee acts as the board's trusted guardian, making sure the financial information shared with shareholders and the public is both honest and transparent.

The Guardian of Financial Integrity

Think of a company as a large ship navigating treacherous financial waters. The audit committee isn't the captain or the crew running day-to-day operations. Instead, they are the expert navigator, completely separate from the action on deck.

Their job is to constantly check the maps, verify the coordinates, and ensure the navigational instruments are accurate. This crucial work helps the ship avoid hidden dangers and reach its destination safely, protecting everyone on board—especially the investors who funded the voyage.

This function has moved far beyond a simple box-ticking exercise. Today, the audit committee is a strategic pillar of corporate governance, absolutely essential for building and maintaining investor trust. Without it, stakeholders would have little independent proof that the company's reported performance is real.

Core Purpose and Strategic Importance

The committee’s main purpose is to serve as a critical check and balance on management. It creates a direct line of communication between the board of directors and both internal and external auditors, fostering an environment where everyone is held accountable.

Its purpose is defined by a few key functions:

- Financial Reporting Oversight: Scrutinizing quarterly and annual financial statements to confirm they are fair, accurate, and follow all applicable rules.

- Auditor Management: Selecting, paying, and overseeing the work of the independent external auditors, making sure their objectivity is never compromised.

- Internal Control and Risk Review: Evaluating how well the company’s internal control systems work and how it manages significant financial risks.

In today's complex business world, a proactive and engaged audit committee isn't just a regulatory requirement—it's a powerful defense against financial misstatement and corporate fraud. Its effectiveness is directly tied to investor confidence and long-term company stability.

The Evolution From Compliance to Strategy

The audit committee was initially seen as a procedural chore. But its responsibilities have expanded dramatically over the years. High-profile corporate scandals revealed the catastrophic fallout from weak oversight, which led to much stricter regulations and higher expectations from the public.

Now, committees are expected to be forward-looking. They anticipate emerging risks rather than just reviewing what already happened.

This shift means the audit committee's role is now deeply strategic. Its members must understand not only accounting principles but also the company’s business model, industry challenges, and complex modern risks like cybersecurity. Their insights help the entire board make smarter decisions, cementing the committee's place as an indispensable part of sound governance.

How Scandals Shaped the Modern Audit Committee

The powerful audit committee role we know today wasn’t born in a quiet boardroom; it was forged in the fire of corporate scandal. For decades, many audit committees were passive, almost ceremonial bodies. They were often seen as a formality rather than a real line of defense against financial misconduct.

That all changed at the turn of the millennium. A series of massive accounting frauds—involving household names like Enron and WorldCom—sent shockwaves through the financial markets. These scandals vaporized billions in investor wealth and, just as importantly, shattered public trust.

The fallout was immense. It became painfully obvious that weak oversight, conflicted auditors, and aggressive accounting had been allowed to fester. Lawmakers had no choice but to act decisively to prevent a repeat of such a catastrophic failure in corporate governance.

The Rise of Regulatory Mandates

In response to the crisis, governments around the world rolled out sweeping legislation. The most famous of these is the Sarbanes-Oxley Act of 2002 (SOX) in the United States. This landmark law completely redefined the responsibilities of public companies, their executives, and their auditors.

SOX transformed the audit committee from a passive advisory group into a legally mandated powerhouse with specific, non-negotiable duties. Suddenly, what had once been considered "best practice" was now the law.

Key changes included:

- Mandatory Independence: SOX required all audit committee members to be independent directors. This meant no financial ties to the company other than their board fees, a rule designed to kill conflicts of interest.

- Financial Expertise: The law mandated that at least one member must be a designated “financial expert,” ensuring the group had the chops to challenge complex accounting.

- Direct Auditor Oversight: The committee was given the sole authority to hire, fire, and oversee the external auditors. This severed the historically cozy relationship between auditors and company management.

These rules fundamentally shifted the balance of power, placing the audit committee squarely at the center of financial oversight and accountability.

A Lasting Impact on Governance

The impact of these scandals and the resulting regulations can't be overstated. They ushered in a new era of accountability where the audit committee role became synonymous with corporate integrity. The heightened scrutiny forced a global refocus on strengthening financial reporting to rebuild investor confidence.

But the journey isn't over. A global survey of over 1,200 audit committee members revealed that nearly 50% rated their committees as only “somewhat effective” or needing improvement. Despite the challenges, there has been clear progress, as about 70% of respondents from the Americas reported their committee had become more effective in the preceding year. You can dig into these evolving governance dynamics in the full survey report.

This history shows exactly why the audit committee holds such a critical position today. Its authority isn't just a matter of good governance; it's a direct consequence of past failures, designed to protect the financial system and ensure that trust, once lost, can be rebuilt.

Unpacking The Core Responsibilities

So, what does an audit committee actually do? We've covered the history, but what happens in the boardroom, quarter after quarter? It's not a single job but a web of overlapping oversight duties that act as a shield for the company’s integrity. Think of the committee as the board's eyes and ears for everything related to financial accuracy and risk.

This isn't just about rubber-stamping reports. It demands a deep, probing engagement with management, auditors, and the systems that keep everything in check. The committee has to ask the tough questions and make sure the answers hold up.

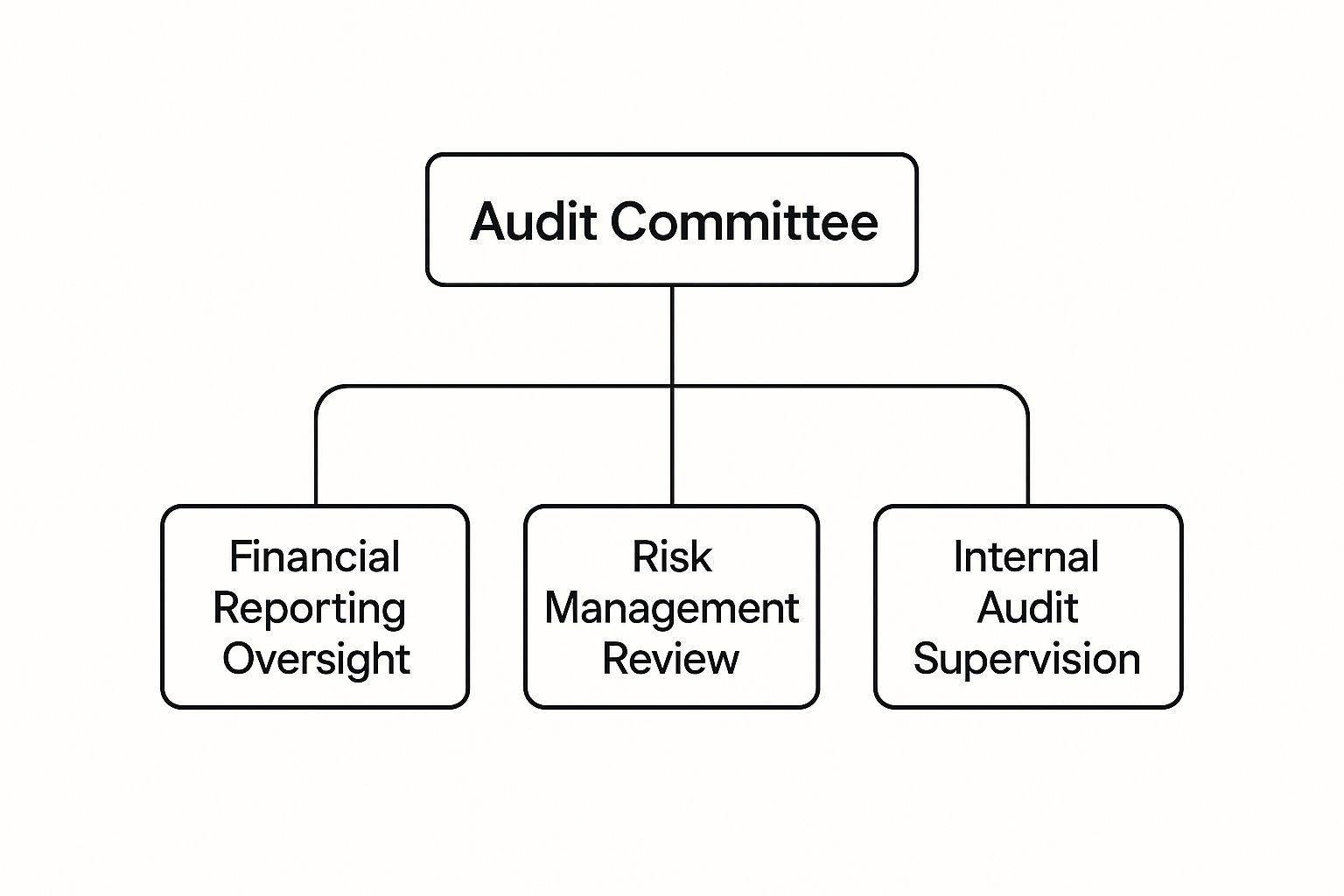

This image neatly breaks down the main pillars of the committee's work.

As you can see, everything rests on three core functions: overseeing financial reporting, managing auditors, and keeping a close watch on internal controls and risks.

To make these duties clearer, here's a quick breakdown of how these responsibilities translate into real-world actions.

Key Responsibilities of the Audit Committee

| Responsibility Area | Primary Focus | Example Activities |

|---|---|---|

| Financial Reporting Oversight | Ensuring financial statements are accurate, transparent, and fair. | – Scrutinizing quarterly and annual financial reports. – Questioning management’s accounting judgments and estimates. – Reviewing earnings releases before they go public. |

| External Auditor Management | Maintaining the independence and performance of the external audit firm. | – Appointing, compensating, and if necessary, firing the external auditors. – Reviewing the annual audit plan and scope. – Discussing audit findings and any disagreements with management. |

| Internal Controls & Risk | Verifying that the systems for financial reporting are sound and effective. | – Evaluating the design and effectiveness of internal control over financial reporting (ICFR). – Overseeing the internal audit function. – Ensuring management addresses any identified control weaknesses. |

| Compliance & Whistleblowing | Upholding legal, regulatory, and ethical standards across the company. | – Monitoring compliance with key laws and regulations. – Overseeing the company’s whistleblower hotline and procedures. – Reviewing any significant legal or ethical investigations. |

Each of these areas is critical. Let's dive a little deeper into what each one entails.

Financial Reporting Oversight

This is the most visible part of the job: making sure the company's financial statements are rock-solid. But it's not a passive review. It means actively questioning and challenging the assumptions and judgments management makes when putting the numbers together.

Committee members need to dig into everything from how revenue is recognized to whether the company has set aside enough money for potential losses. The goal isn't just to be technically correct; it's to ensure the financials present a fair and transparent picture of the company's health. This includes reviewing quarterly earnings releases and any other financial information shared with investors and the public.

Managing the External Auditors

A huge part of the audit committee role is its direct and exclusive authority over the external auditors. This relationship is the bedrock of auditor independence. The committee is solely responsible for a few key actions.

- Appointment and Compensation: It chooses the independent audit firm and negotiates their fees. This takes management out of the equation and prevents any potential conflicts of interest.

- Performance Evaluation: It regularly assesses the audit firm’s work, qualifications, and independence to make sure they're still effective and unbiased.

- Oversight of Audit Work: The committee reviews the scope of the annual audit and discusses any big findings, disagreements with management, or roadblocks the auditors hit along the way.

This direct line of command ensures the auditors answer to a body whose first loyalty is to the shareholders, not to the executives whose work they are checking.

Reviewing Internal Controls and Risk Management

Beyond the numbers themselves, the audit committee has to look at the systems that produce them. It oversees the company's internal control over financial reporting (ICFR)—all the processes and procedures designed to prevent or catch major errors or fraud.

Think of it this way: they’re not just inspecting the final product, but the factory's entire quality control system.

The committee evaluates how well these controls are working, often with help from both internal and external auditors. If weaknesses are found, the committee is on the hook to make sure management fixes them—fast. This proactive stance helps stop small financial issues before they balloon into disasters.

A strong internal control framework is the bedrock of reliable financial reporting. The audit committee’s job is to make sure that bedrock is solid, with no cracks that could compromise the company's integrity.

Overseeing Compliance and Whistleblower Programs

The modern audit committee’s job has grown well beyond traditional finance. Today, its duties often include overseeing the company's compliance with laws and regulations. This means understanding the legal landscape the business operates in and confirming that solid processes are in place to stay on the right side of the law.

On top of that, the committee is usually responsible for setting up and overseeing procedures for handling complaints—especially those related to accounting, internal controls, or auditing. This includes managing the company's whistleblower hotline, which gives employees a safe and confidential way to report concerns without fear of retaliation. It’s an essential early warning system for potential trouble.

The scope of these duties just keeps expanding. A recent survey found that 80% of audit committees now oversee legal and regulatory compliance, and 70% are responsible for data governance. Despite this, only 51% of committee members feel confident in their ability to communicate these activities to stakeholders. To get better, 56% said they needed more and better information from management.

These numbers tell a clear story: the audit committee's role is constantly evolving. As you can discover insights from the 2023 Global Audit Committee Survey, there's a growing need for committees to adapt, learn, and improve how they communicate to meet ever-increasing expectations.

Building an Independent and Expert Committee

An audit committee is only as good as the people sitting around the table. The whole point of modern corporate governance hinges on two absolute must-haves for its members: independence and expertise. These aren’t just nice ideas; they’re hard rules designed to make sure the committee can do its job without bias or blind spots.

The bedrock principle is total independence from the company's management. Picture it like a firewall between the committee and the C-suite. Members can't be executives, employees, or have any other major financial ties to the company beyond their director's pay.

This separation isn't negotiable. Having a CEO or CFO on the audit committee would be like letting a student grade their own exam—it creates an instant conflict of interest that kills the purpose of oversight. The committee has to be able to challenge management’s decisions with a clear, objective eye, which is impossible if its members are on the same team they’re supposed to be watching.

The Anatomy of an Effective Committee

Laws like the Sarbanes-Oxley Act lay down clear rules for who can be on the committee, reinforcing this independence and setting a baseline for competence. While the details might differ slightly, the blueprint for most public companies is pretty standard.

- Size: Most audit committees have at least three members. This brings a mix of perspectives to the table without getting too crowded for quick, decisive action.

- Independence: Every single member must be an independent director, as defined by the rules of their stock exchange. No exceptions.

- Financial Literacy: All members need to be "financially literate," which just means they can read and understand basic financial statements. This is the ticket to entry for everyone on the team.

This setup ensures the committee has the collective horsepower to handle its crucial audit committee role. The financial literacy rule guarantees that every member can actually follow the conversation when complex financial reports are on the table. For anyone looking to get up to speed or sharpen their skills, there are specialized courses available. Continuous learning is a big part of the job, and tailored training for directors can help members stay on top of their game.

Demystifying the Role of the Financial Expert

On top of general financial literacy, regulations also require at least one person on the committee to be officially named the "audit committee financial expert." This label causes a lot of confusion. It doesn't mean they have to be a CPA or a former auditor, though many are.

A financial expert is someone who can do more than just read the numbers—they understand the story the numbers are telling. They have the experience to question tricky accounting methods, push back on management’s assumptions, and spot potential red flags that others might not see.

This kind of know-how usually comes from experience as a public accountant, CFO, controller, or a similar senior financial job. Their role on the committee is indispensable. They act as the guide, helping other members make sense of sophisticated issues like derivatives, revenue recognition policies, or the financial fallout of a major acquisition. This expert leadership ensures the committee can go toe-to-toe with both auditors and management, asking the sharp, informed questions that are the heart and soul of strong oversight.

A Playbook for High-Impact Audit Committees

Knowing the duties of an audit committee is one thing; mastering the art of high-impact oversight is another. Moving from just meeting compliance requirements to genuine excellence demands a deliberate strategy. It’s a playbook of proven practices that turns a good committee into a great one. This is the difference between simply checking boxes and truly safeguarding the organization.

The foundation of this playbook is a culture of constructive skepticism. This isn't about being cynical or adversarial. It’s about maintaining a curious, questioning mindset that challenges assumptions and probes for a deeper understanding, making sure every report and assertion is robustly tested.

This culture thrives on open dialogue. Members must feel empowered to ask tough questions, and management must feel obligated to provide transparent answers. A high-impact committee doesn’t just sit through presentations; it drives a dynamic conversation that gets to the heart of the matter.

Fostering a Culture of Rigorous Inquiry

The best committees are defined by the quality of their discussions, not the length of their meetings. They create an environment where no topic is off-limits and every member’s voice is heard. This takes intentional effort from the committee chair to manage agendas, encourage everyone to participate, and protect the space for candid debate.

A recent survey highlights this perfectly. While 89% of audit committee members believe their meetings give them enough time for agenda items, 65% see clear room for improvement. The top suggestion, cited by 29% of them, was to increase engagement and substantive discussion. You can explore how top committees are raising their game in the latest governance report.

This data shows that just following procedure isn't enough. The real value is unlocked when members arrive fully prepared, having thoroughly reviewed all materials. It's about fostering an atmosphere where challenging management’s judgments isn’t just accepted—it's expected.

A truly effective audit committee meeting should feel less like a formal presentation and more like a strategic workshop, where complex issues are dissected and potential risks are collaboratively identified and addressed.

The Power of Private Sessions

One of the most powerful tools in the committee’s playbook is the private executive session. These are confidential meetings held without any members of company management present. They create a unique opportunity for the committee to have completely unvarnished conversations with key players.

Holding separate private sessions with the following groups is a critical best practice:

- The External Auditors: To discuss any concerns about management’s cooperation, accounting practices, or potential disagreements without fear of reprisal.

- The Head of Internal Audit: To get an unfiltered view of the company’s internal control environment and any pressures the internal audit team may be facing.

- The General Counsel: To discuss significant legal matters or compliance investigations that might have financial implications.

These sessions are where the unvarnished truth often emerges. They give the committee insights it would never get in a full group setting.

Embracing Continuous Learning

The business landscape is constantly shifting, bringing new and complex risks to the forefront. A static audit committee will quickly become an obsolete one. High-impact committees commit to continuous learning to stay ahead of emerging threats.

This means actively seeking education on topics that go far beyond traditional accounting. Today, that includes understanding the nuances of cybersecurity, the complexities of Environmental, Social, and Governance (ESG) reporting, and the implications of new technologies like artificial intelligence. As risks evolve, so must the committee’s expertise. For example, staying current with electronic discovery services is crucial for overseeing litigation risks effectively.

By dedicating time to education, the committee not only sharpens its own oversight capabilities but also signals to the entire organization that these emerging risks are a top priority. This proactive stance ensures the audit committee role remains a cornerstone of forward-thinking governance.

How to Measure Committee Effectiveness

A great audit committee doesn't just go through the motions. It constantly looks for ways to get better. But how can a committee honestly size up its own performance? The key is to move past simple checklists and dig into what really matters.

Effective measurement isn't about ticking boxes to prove you did the work. It’s about genuine introspection and a frank self-assessment of the quality of discussions, the depth of risk oversight, and the committee’s actual contribution to corporate integrity.

Moving Beyond Compliance Checklists

Compliance is the floor, not the ceiling. Of course, following regulations is non-negotiable, but a top-tier committee measures its value by the quality of its engagement and its proactive influence on governance.

This demands a shift in mindset. You have to stop asking, "Did we cover everything?" and start asking, "Did we challenge assumptions and add real value?" The aim is to build a culture of continuous improvement where self-evaluation is a natural part of the committee's annual cycle.

A structured, annual self-assessment is one of the best tools for this. The process usually kicks off with a detailed questionnaire that each member completes anonymously. This is followed by a candid group discussion to talk through the results.

Key Areas for Self-Assessment

To be truly useful, a self-assessment has to ask probing, practical questions that get to the heart of how the committee actually operates. The evaluation should zoom in on a few key performance indicators.

- Meeting Dynamics: Are agendas focused on the most critical risks? Do meetings leave enough room for deep discussion, or are they just a series of one-sided presentations?

- Information Quality: Is the material from management clear, concise, and delivered with enough time for a proper review? Does it actually enable a strategic conversation?

- Member Engagement: Does every member actively participate? Do they ask the tough questions and contribute their unique expertise? Is there a culture of healthy skepticism in the room?

- Risk Oversight Effectiveness: How well does the committee grasp emerging threats like cybersecurity and ESG? Does it effectively challenge the company's strategies for managing these risks? A crucial piece of this is understanding complex areas like legal risk management in eDiscovery to ensure nothing falls through the cracks.

The ultimate measure of an audit committee's effectiveness is its ability to foster an environment of transparency and accountability, ensuring that difficult conversations happen before they become headline news.

Answering these questions honestly helps pinpoint specific weaknesses. For example, if the pre-read materials are consistently falling short, that’s a clear signal to demand better from management. In fact, one recent survey found that improving the quality of meeting presentations and pre-reads were top suggestions for boosting committee performance.

This kind of self-reflection creates a clear roadmap for improvement. It ensures the audit committee role remains a dynamic and powerful force for good governance, continually adapting to protect the organization and its stakeholders.

Got Questions About the Audit Committee?

Even for seasoned board members, the practical side of the audit committee role can bring up a few questions. Let's break down some of the most common ones that come up in the boardroom.

How Does It Work With Other Board Committees?

The audit committee definitely isn’t a solo act. It has to work hand-in-glove with other key groups, like the compensation and governance committees, to make sure oversight is seamless.

Think of it this way: the audit committee might team up with the compensation committee to scrutinize executive expense reports or huddle with the governance committee to sharpen the company's whistleblower policy. This kind of teamwork prevents blind spots and ensures that critical risks are managed cohesively across the entire board.

What Skills Are Essential for Members?

While having a designated "financial expert" is a must, a truly great committee is more than just numbers people. It's a blend of different strengths.

Beyond being fluent in accounting, here are a few skills that make a huge difference:

- Deep Industry Know-How: You need people who understand the unique operational and financial risks that come with your specific sector.

- A Knack for Risk Management: This means being able to spot emerging threats and challenge management’s plans for dealing with them.

- Cybersecurity Smarts: This is no longer a "nice-to-have." With 50% of committees now ranking cybersecurity as their top priority, it's become a core competency.

The best committees combine deep financial expertise with broad business judgment. It’s this mix that allows them to connect the dots between the numbers on a page and the company's real-world strategy and risks.

What Is Its Role in Whistleblower Programs?

The audit committee is the ultimate guardian of the whistleblower program. Its job is to set up rock-solid procedures so employees can report concerns about accounting or auditing—confidentially and anonymously.

But it doesn't stop there. The committee also has to make sure every credible complaint gets a thorough investigation and that real action is taken. This function acts as a critical early warning system, helping to catch potential misconduct before it blows up into a full-blown crisis and cementing a culture of integrity.

At Tascon Legal & Ediscovery, we specialize in giving legal and governance professionals the tools and training they need for effective oversight. We provide end-to-end support that saves time, cuts down on risk, and builds stronger corporate integrity. Find out more about our services at https://tasconlegal.com.