At its heart, the audit committee function is all about providing independent oversight. Think of it as the board's designated watchdog, tasked with making sure a company's financial reporting, internal controls, and audit processes are all above board. This committee serves as a crucial check and balance on management, ensuring the integrity and accuracy of the financial story told to investors and the public.

The Guardian of Corporate Integrity

In any large organization, the audit committee is really the bedrock of investor confidence and corporate accountability. It’s a small, specialized subcommittee of the Board of Directors, but its mission directly impacts the company’s reputation and financial stability. Without this layer of independent oversight, stakeholders would have very little assurance that the financial statements are a true reflection of the company's performance.

The responsibilities of these committees have ballooned over the years. Following a string of major financial scandals in the late 1990s and early 2000s, audit committees were thrust into the spotlight. Their role was transformed from a somewhat passive review board into a much more active, hands-on supervisory body.

A Foundation of Trust and Accountability

The primary job of the audit committee is to safeguard the integrity of the company's financial reporting. It accomplishes this through a few key activities that build a strong culture of accountability from the top down:

- Overseeing Financial Reporting: The committee digs into the annual audited financial statements and quarterly reports, discussing them with both management and the external auditors.

- Supervising the Auditors: It holds the sole authority to hire, pay, and oversee the independent external auditors. This ensures their objectivity isn't compromised.

- Monitoring Internal Controls: The committee constantly evaluates how effective the company’s internal control systems are at protecting assets and sniffing out fraud.

This setup creates a vital separation between the people preparing the financial information (management) and those verifying it (the auditors), with the committee acting as the impartial referee. By understanding the essentials of the audit committee role and its importance, organizations can truly appreciate its value in maintaining corporate health.

An audit committee's effectiveness isn't just about ticking compliance boxes. It's about fostering a culture where transparency and ethical behavior are non-negotiable. It's the first line of defense against financial mismanagement.

Pablo Tascon

A global survey of over 1,200 audit committee members offered a dose of reality. While nearly 70% in the Americas felt their committees had become more effective, the progress isn't universal. Almost half still rated their committees as only “somewhat effective” or in need of improvement, which just goes to show that vigilance is a continuous effort. You can dig deeper into these findings on audit committee effectiveness.

Understanding Core Committee Responsibilities

To really get what an audit committee does, we have to look past the mission statement and dig into its actual, non-negotiable duties. These aren't just boxes to tick on a list; they are active, ongoing processes that form the very backbone of a company’s financial governance. Each responsibility is designed to create a system of checks and balances that keeps management accountable and protects everyone with a stake in the company.

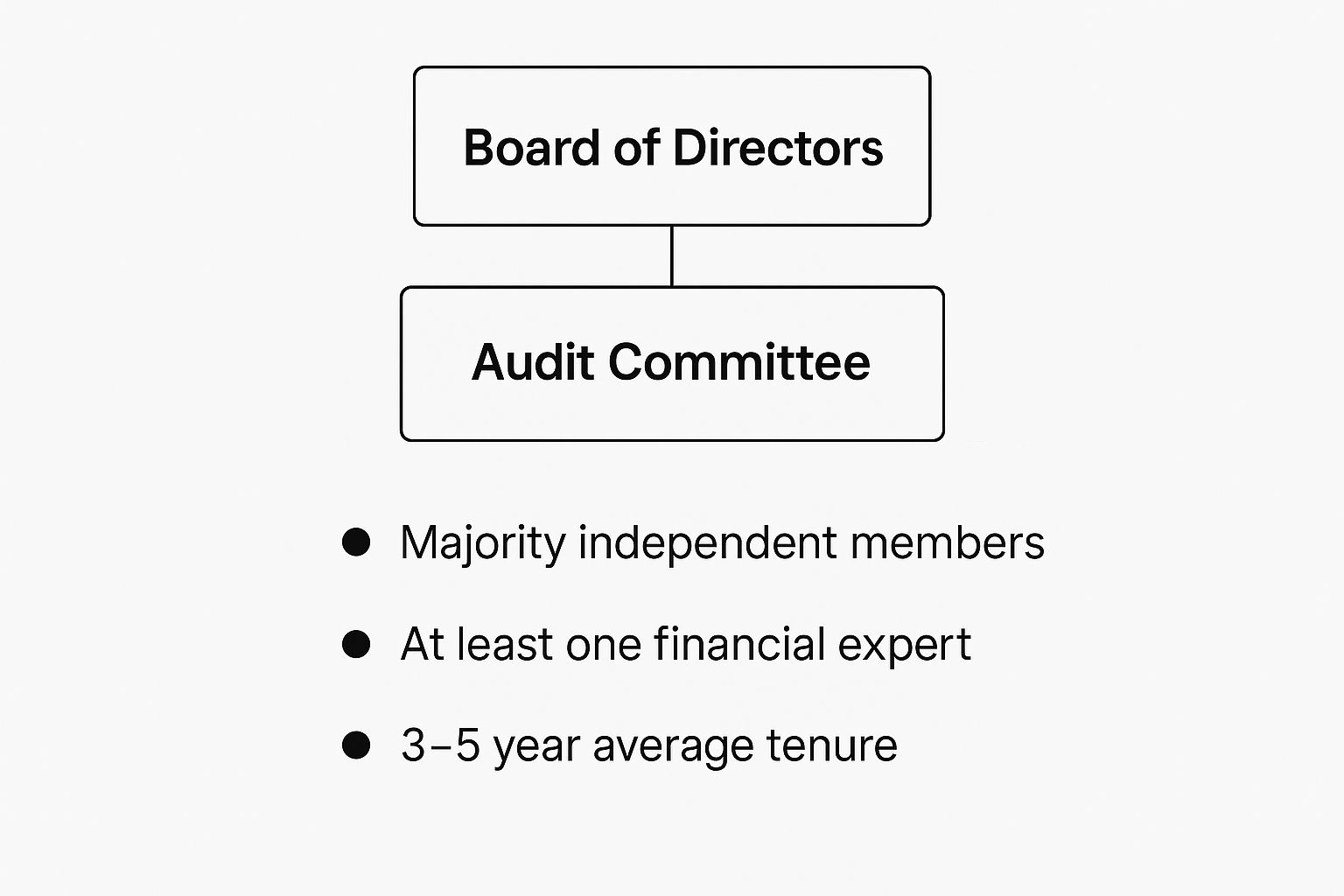

The way the committee is built is absolutely foundational to its success. The best ones are structured with a few key attributes in mind.

This structure is what gives the committee the independence and financial know-how it needs to do its job right. Without it, the whole oversight function falls apart.

Financial Reporting Oversight

The most visible job of the audit committee is keeping a close watch on the financial statements. Before any quarterly or annual report ever sees the light of day, the committee pores over it. They sit down with management and the external auditors to talk through the results, discuss the big judgment calls, and question the accounting principles used.

This is where the tough questions get asked. They might challenge why the company chose a specific method for recognizing revenue or dig into the assumptions behind a major asset valuation. Their goal is simple: make sure the financials paint a true and fair picture of the company’s health, without any major errors or omissions.

Selecting and Supervising the External Auditor

One of the audit committee's most critical powers is its exclusive authority over the external auditor. The committee is the only body responsible for hiring, paying, and—if it comes to it—firing the independent audit firm. This is a huge deal. It completely removes the potential for management to pressure or influence the auditor’s opinion, which is a vital safeguard against biased reporting.

But the relationship goes deeper than just hiring and firing. The committee meets with the auditors regularly, often without anyone from management in the room. This gives them a chance to discuss the audit’s scope, any roadblocks the auditors hit, or disagreements they had with the leadership team. This direct, private line of communication ensures the auditors can be completely candid without fearing any blowback.

An audit committee's true power lies in its independence. By controlling the relationship with the external auditor, it ensures that the firm’s loyalty is to the shareholders, not to the executives whose work they are reviewing.

Pablo Tascon

Reviewing Internal Controls

Finally, the committee is in charge of overseeing the company's internal controls over financial reporting (ICFR). Think of ICFR as the whole system of processes and procedures designed to stop errors and fraud in their tracks—things like requiring two signatures on big payments or making sure bank accounts are reconciled on a regular basis.

The committee reviews management's own assessment of these controls and talks through any weak spots with both the internal and external auditors. A strong system of internal controls is the first line of defense against financial shenanigans. In fact, a shocking number of corporate fraud cases can be traced straight back to weak or overridden controls. By focusing here, the audit committee helps fortify the company from the inside out.

Let's break down these core duties and why they matter in a bit more detail.

Key Responsibilities and Their Purpose

The table below summarises the audit committee's main duties, connecting each area of responsibility to its ultimate purpose.

| Responsibility Area | Primary Objective | Key Activities |

|---|---|---|

| Financial Reporting | Ensure accuracy and transparency of financial statements. | Review quarterly/annual reports, challenge accounting choices, discuss significant estimates. |

| External Auditor Oversight | Maintain auditor independence and audit quality. | Hire, compensate, and fire the auditor; pre-approve services; hold private meetings. |

| Internal Controls (ICFR) | Prevent and detect financial errors and fraud. | Review management’s assessment of controls, discuss weaknesses with auditors. |

| Risk Management | Oversee major financial and compliance risks. | Review risk assessment processes, ensure mitigation plans are in place. |

| Compliance & Ethics | Promote a culture of integrity and legal adherence. | Oversee whistleblower programs, review legal matters, monitor ethics policies. |

Ultimately, each of these functions works together to build a strong governance framework that protects the company and its investors from financial risk and misconduct.

Navigating Risks Beyond Financial Reporting

While financial statements are still the bedrock of its work, the modern audit committee is looking far beyond the ledger. Its scope has stretched to cover a complex and shifting landscape of non-financial threats that can hit the bottom line just as hard. It’s no longer just about the numbers; it’s about organizational resilience.

This shift happened because a company’s biggest weak spots often have nothing to do with traditional accounting. A massive data breach, a critical system failure, or a steep regulatory fine can cripple a business just as effectively as a financial misstatement. The committee now has to be a guardian against a much wider array of dangers.

Expanding Oversight to Cybersecurity

Cybersecurity has shot to the top of nearly every audit committee's agenda, and for good reason. A recent survey showed that 93% of audit committee members rank cybersecurity as one of their top three concerns. That intense focus is a direct response to the severe financial and reputational damage a single security slip-up can cause.

The committee’s job isn’t to become a group of cybersecurity experts. Instead, they provide high-level oversight by asking the tough questions:

- Risk Assessment: Is management actually identifying and sizing up the most serious cyber threats to the organization?

- Resource Allocation: Is there enough money and people dedicated to protecting our most critical digital assets?

- Incident Response: Do we have a clear, tested plan to manage and recover from a cyberattack if one happens?

By pushing for solid answers, the committee helps build a much stronger defense against digital threats that could destabilize the whole company.

The audit committee's responsibility is to ensure that cybersecurity risk is not just an IT problem, but a core business risk that is managed with the same rigor as financial or operational risks.

Pablo Tascon

The Rise of Enterprise Risk Management (ERM)

Beyond specific threats like cyberattacks, committees are increasingly tasked with overseeing the company's entire Enterprise Risk Management (ERM) program. Think of ERM as a holistic approach that tries to spot, assess, and prepare for anything that could get in the way of the organization's goals.

This means the audit committee is now looking at everything from supply chain disruptions and geopolitical instability to regulatory changes and even talent shortages. This wider view helps connect the dots between different kinds of risks, stopping the organization from operating in silos. For instance, effectively managing contract risk is a crucial part of any good ERM framework, as it can head off major financial liabilities down the road.

A Broader Mandate Confirmed by Data

This expanded oversight isn't just an emerging trend; it's the new standard. A 2023 global survey confirmed that audit committees have major responsibilities well beyond the financial audit. The report found that 80% of respondents said legal and regulatory compliance was a huge part of their oversight, and 70% pointed to data governance as a key focus area. You can dig into the specifics in the full survey from KPMG on global audit committee insights.

Building an Effective Audit Committee

An audit committee that just ticks the compliance boxes is like a car that only has an engine—it might run, but it won’t get you very far. A truly high-performing committee, on the other hand, is deliberately built with the right parts, the right people, and the right leadership. This intentional design is what turns the audit committee from a simple oversight body into a powerful strategic asset for the company.

To get there, you have to start with three non-negotiable pillars: independence, financial literacy, and diverse expertise. Every single member must be independent, meaning they have no significant ties to the company outside of their board seat. This objectivity is the bedrock of their ability to challenge management without holding back.

On top of that, every member needs to be financially literate. They have to be able to pick up a set of financial statements and understand what they're looking at. Without that baseline knowledge, effective oversight is simply impossible.

Assembling the Right Mix of Skills

While financial literacy is the price of entry, a high-impact committee needs a lot more than just accounting basics. The real goal is to build a team with a blend of skills that directly mirrors the company’s biggest risks. Think of it like assembling a specialist team for a complex mission—you need different experts to cover all your bases.

This means you should be actively looking for members with specific backgrounds, like:

- A Designated Financial Expert: You need at least one person who has lived and breathed accounting or financial management, often a former CFO or a retired audit partner.

- Industry Veterans: Someone who deeply understands the operational hurdles and regulatory minefields in your specific sector brings invaluable context that numbers alone can't provide.

- Technology and Cybersecurity Specialists: With digital threats being what they are today, having a member who can fluently discuss IT risk is no longer a "nice-to-have." In fact, a recent survey found that 31% of audit committee members believe cybersecurity expertise is the single most important skill needed to make their committees better.

Getting this mix right ensures the committee can ask the tough, insightful questions needed for robust oversight across all the areas that matter. To make sure your directors are up to the task, ongoing education is essential, and specialized training for directors can be a great way to fill any critical knowledge gaps.

The Importance of Structure and Leadership

The sweet spot for committee size is usually between three and five members. That’s large enough to bring in different perspectives but small enough to stay nimble and allow for real, in-depth discussion. A committee that’s too big can get bogged down, while one that’s too small might not have the bandwidth or range of expertise to get the job done right.

The strength of an audit committee is not just in its individual members, but in its collective ability to operate as a cohesive, inquisitive, and courageous unit. This synergy is cultivated by a strong and independent chair.

Pablo Tascon

The committee chair is the absolute linchpin. A great chair sets the tone, drives the agenda, and creates an environment where open dialogue and healthy skepticism can thrive. They need to be a skilled facilitator, making sure meetings are focused on the big strategic risks, not just routine compliance checks. Without that steady hand at the helm, even a committee full of all-stars can struggle to fulfill its mission.

Strategies for Maximizing Committee Effectiveness

Getting the right people with the right skills in the room is just the starting line. But structure alone doesn't create a high-impact audit committee—execution is what separates the good from the great. It all comes down to a deliberate approach to running meetings, building relationships, and never stop improving.

This shift from simply having a committee to making it truly effective is critical. The world of risk is always changing, and so are the responsibilities of the audit committee. A 2023 Deloitte survey highlighted this perfectly: two-thirds of respondents felt their committee had room to grow, and only one-third believed their committees were as effective as they could be. The big opportunities for improvement? Sharper meeting agendas and more candid, open conversations. You can dig into the full findings on audit committee effectiveness to see the details.

Conducting Purposeful and Strategic Meetings

Effective meetings are the engine of a high-performing audit committee. Too often, though, agendas get stuck in a rut—a repetitive cycle of compliance box-ticking that leaves no time for the real strategic discussions. The best committees flip this script. They design their meetings to focus on forward-looking risks and the critical judgments that matter most.

How do they pull this off? The committee chair has to be proactive, working closely with management and the auditors to set a dynamic agenda. Forget about long, droning presentations. Instead, materials are sent out well ahead of time. This frees up the meeting itself for what it’s supposed to be about: robust debate and tough questions. It transforms the meeting from a passive reporting session into an active oversight workshop where real value gets created.

Cultivating Key Stakeholder Relationships

An audit committee can't operate in a vacuum. Its success is built on the strength of its relationships with three crucial groups: management, internal auditors, and external auditors. In this world, trust and open communication are everything.

Building these relationships takes work, and it happens outside the boardroom. The committee chair should have regular, informal check-ins with the CFO, the Chief Audit Executive (CAE), and the lead audit partner. These aren't formal meetings; they're conversations that build rapport and open up channels to raise concerns early, long before they snowball into major problems.

A committee that only interacts with its stakeholders during quarterly meetings is operating with blinders on. The real work happens in the continuous, candid dialogue that builds trust and ensures an unfiltered flow of information.

Pablo Tascon

When these relationships are strong, the committee can do its job far more effectively. Here’s what it looks like in practice:

- With Management: It creates an environment where the committee can challenge assumptions without putting everyone on the defensive.

- With Internal Audit: It guarantees the committee gets independent, straight-from-the-source assessments of internal controls and risk management.

- With External Audit: It ensures the auditors feel supported and empowered to maintain their professional skepticism and do their jobs without interference.

Embracing Continuous Improvement

The most effective audit committees are never satisfied with the status quo. They know the risk landscape is in constant motion, and their skills and processes have to keep up. This commitment to getting better shows up in two key practices: continuous education and regular self-evaluations.

Committee members need ongoing training to stay sharp on emerging topics like cybersecurity, data analytics, and new accounting standards. Just as important, the committee must conduct an annual self-assessment to take an honest look in the mirror. This evaluation should ask the tough questions, pinpoint weaknesses, and result in a concrete, actionable plan for improvement in the year ahead.

Common Questions About the Audit Committee

Even for experienced executives and board members, the inner workings of an audit committee can raise a few questions. Getting clear on these common points is the key to understanding just how vital the audit committee function really is. Let’s tackle some of the most frequently asked questions head-on.

What Is the Difference Between Internal and External Audit?

It's easy to get these two mixed up, but their roles are fundamentally different.

Think of it like this: internal audit is the company’s own quality control team. They’re part of the organization, and their job is to provide independent assurance that the company’s risk management, governance, and internal controls are working as they should. They help the business get better from the inside out.

External audit, on the other hand, is like an independent, third-party inspector. They're brought in from an outside firm to give a formal, unbiased opinion on whether the company's financial statements are accurate and free of major errors.

The audit committee oversees both, but one is focused on internal improvement, and the other is all about external validation.

How Does an Audit Committee Remain Independent?

Independence isn’t just a buzzword; it’s the bedrock of an effective audit committee. Several strict practices keep it that way.

First, regulations require all committee members to be independent directors. This means they have no significant financial or personal ties to the company that could cloud their judgment or create a conflict of interest.

Second, the committee regularly holds private executive sessions with the internal and external auditors—without any management present. This creates a space for completely candid, unfiltered conversations about any issues or concerns that might otherwise go unsaid.

Finally, the committee has the sole authority to hire, pay, and oversee the external auditor. This structural firewall prevents management from putting pressure on the audit relationship, ensuring the auditor’s true allegiance is to the shareholders, not the C-suite.

What Qualifications Should an Audit Committee Member Have?

You need the right expertise in the room for oversight to mean anything. At a bare minimum, every member must be financially literate. This means they can read and understand fundamental financial statements like the balance sheet and income statement without needing a translator.

Beyond that baseline, regulations often demand at least one member be a designated "financial expert." This is typically someone with deep experience in accounting or finance, like a former CFO or a certified public accountant.

But today, the game has changed. Committees are actively looking for members whose skills reflect modern business risks. Expertise in cybersecurity, technology, or specific industry regulations is becoming just as critical as traditional financial acumen.

Pablo Tascon

How Often Does the Audit Committee Typically Meet?

The rhythm of audit committee meetings is set by the company's reporting calendar and its specific risk profile. Most committees meet at least four times a year, which lines up perfectly with the review of quarterly and annual financial reports.

But that’s just the starting point.

For a complex company operating in a high-risk industry, meeting more often is standard practice. Special sessions might also be called to deal with urgent issues as they arise, like a significant whistleblower complaint, a major breakdown in internal controls, or a newly discovered cybersecurity breach. The goal is simple: meet often enough to give every critical issue the time and attention it deserves.

At Tascon Legal & Ediscovery, we understand the complexities of corporate governance and the critical need for effective oversight. We provide end-to-end support that helps organizations streamline their legal operations, from sourcing top UK-qualified legal talent to delivering training that upskills your teams. Find out how we can help you reduce risk and maximize ROI at https://tasconlegal.com.